Contents

The digital age has ushered in an era of unprecedented connectivity and technological advancement, transforming nearly every aspect of human life and commerce. While these innovations offer immense opportunities, they also present a fertile ground for new and evolving forms of illicit activities, particularly cybercrime and financial fraud. The increasing sophistication of cybercriminals, coupled with the globalized nature of financial transactions, has created a complex landscape where traditional accounting and auditing methods often fall short. In this challenging environment, forensic accounting has emerged as an indispensable discipline, combining accounting, auditing, and investigative skills to detect, prevent, and respond to financial misconduct.

Forensic accounting is no longer confined to analyzing paper trails; it has evolved to encompass the intricate digital footprints left by financial transactions in the cyber realm. From tracing illicit cryptocurrency flows to unraveling complex ransomware schemes and business email compromise (BEC) attacks, forensic accountants are at the forefront of combating financial crime in the digital era.

This Forensic Accounting in the Digital Era essay dives into the critical role of forensic accounting in this evolving landscape, exploring its methodologies, the current trends in cybercrime and financial fraud, prominent case studies, and the future challenges and opportunities for the profession. By understanding the intersection of technology, crime, and financial investigation, we can better appreciate the vital contribution of forensic accounting in safeguarding economic integrity and ensuring justice in an increasingly digital world.

The Evolution of Forensic Accounting

Forensic accounting, while gaining significant prominence in the digital era, is not a new discipline. Its roots can be traced back to the early 20th century, with some even pointing to the investigation of Al Capone by the IRS as an early example of financial investigation leading to legal prosecution. However, the scope and methodologies of forensic accounting have undergone a profound transformation, particularly with the advent of information technology and the internet.

Historically, forensic accounting primarily involved meticulous examination of physical documents such as ledgers, invoices, bank statements, and contracts. Investigations were often labor-intensive, relying on manual reconciliation and analysis to uncover discrepancies, anomalies, and patterns indicative of fraud. The focus was largely on traditional financial crimes like embezzlement, misappropriation of assets, and financial statement fraud within a localized, paper-based environment.

The digital revolution, however, has fundamentally reshaped the financial landscape. The widespread adoption of electronic transactions, digital record-keeping, and interconnected global financial systems has created both new opportunities for legitimate commerce and unprecedented avenues for illicit activities. This shift necessitated a corresponding evolution in forensic accounting practices. The traditional ‘follow the money’ approach now requires forensic accountants to ‘follow the data,’ navigating complex digital environments to uncover hidden financial trails.

This evolution has led to the integration of digital forensics into the core competencies of forensic accounting. Digital forensics involves the collection, preservation, analysis, and presentation of digital evidence. For forensic accountants, this means working with data from a myriad of sources, including:

- Enterprise Resource Planning (ERP) systems: Comprehensive software suites that manage all aspects of a business, from accounting and human resources to supply chain and customer relations, generating vast amounts of financial data.

- Customer Relationship Management (CRM) systems: Databases containing customer interactions and sales data, which can reveal patterns of fraudulent sales or customer manipulation.

- Email and communication records: Often contain crucial evidence of fraudulent schemes, collusion, or instructions for illicit transactions.

- Cloud-based storage: Increasingly used for storing financial records and communications, requiring specialized techniques for data retrieval and analysis.

- Mobile devices: Smartphones and tablets can hold significant financial data, communication logs, and transactional information relevant to an investigation.

- Blockchain and cryptocurrency ledgers: The emergence of cryptocurrencies has introduced a new layer of complexity, requiring expertise in blockchain analysis to trace illicit funds.

The transition from physical to digital evidence has also brought new challenges, including the sheer volume of data, the need for specialized software and tools, and the imperative to maintain data integrity and chain of custody in a digital environment. Consequently, modern forensic accountants must possess a blend of traditional accounting acumen, investigative skills, and a strong understanding of information technology and cybersecurity principles. This interdisciplinary approach is essential for effectively combating the sophisticated financial crimes prevalent in the digital era.

Beat Your Deadline

Hire a Writer Today!

✅ Get Your Assignment Done by Experts

The Current Landscape of Cybercrime and Financial Fraud

The digital era has not only transformed legitimate business operations but has also provided new avenues and tools for criminals to perpetrate sophisticated cybercrimes and financial frauds. The scale and complexity of these illicit activities are growing at an alarming rate, posing significant threats to individuals, businesses, and national economies worldwide. Understanding the current landscape is crucial for developing effective countermeasures.

Cybercrime Statistics and Trends

Cybercrime is a rapidly expanding global threat. Recent data highlights the pervasive nature and escalating costs associated with cyberattacks:

- Widespread Impact: In 2023, approximately 50% of UK businesses reported experiencing some form of cyberattack. Globally, cyberattacks surged by 125% in 2021 compared to 2020, with this upward trend continuing into 2022 [1].

- Dominance of Phishing: Phishing remains the most prevalent form of cybercrime. In 2021, 323,972 internet users fell victim to phishing attacks, accounting for half of all data breaches. The COVID-19 pandemic exacerbated this trend, with phishing incidents increasing by 220%. The exposure of nearly 1 billion emails in 2021, affecting one in five internet users, partly explains the continued effectiveness of phishing campaigns [1].

- Ransomware Epidemic: Ransomware attacks continue to be a severe threat, with approximately 236.1 million attacks reported globally in the first half of 2022. These attacks often involve encrypting critical data and demanding cryptocurrency payments for its release, disrupting operations and causing substantial financial losses [1].

- Escalating Data Breach Costs: The financial repercussions of data breaches are soaring. Since 2001, the hourly victim count has surged by 1517%, from 6 victims per hour to 97. Concurrently, the average hourly cost of data breaches worldwide escalated from 2, 054in2001toastaggering787,671 in 2021 [1]. Significant

- Financial Losses: In 2022, data breaches cost businesses an average of 4.35million.Investmentfraudemergedasthemostcostlycybercrimein2022, withvictimslosinganaverageof 70,811 per incident [1].

- Vulnerability of Small and Medium-sized Businesses (SMBs): A concerning 67% of SMBs report lacking the in-house expertise to manage data breaches effectively. However, there is a positive trend towards collaboration, with 89% of SMBs engaging Managed Service Providers for cybersecurity in 2022, up from 74% in 2020 [1].

- Geographic Disparities: In 2021, Asian organizations bore the brunt of cyberattacks (26%), followed closely by Europe (24%) and North America (23%). The UK recorded the highest number of cybercrime victims per million internet users in 2022, with 4,783, marking a 40% increase over 2020 figures [1].

- Future Projections: The financial toll of cybercrime is projected to reach an astounding $10.5 trillion annually by 2025, underscoring the urgent need for enhanced cybersecurity measures and proactive forensic interventions [1].

Financial Fraud Statistics and Trends

Financial fraud, often intertwined with cybercrime, presents another formidable challenge. The Federal Trade Commission (FTC) reported a significant increase in consumer losses due to fraud:

- Mounting Losses: Consumers reported losing over $12.5 billion to fraud in 2024, representing a 25% increase from the previous year. This surge is attributed not to an increase in the number of fraud reports, but rather to a higher percentage of victims experiencing financial losses (38% in 2024 compared to 27% in 2023) [2].

- Investment Scams as a Major Threat: Investment scams were the most financially damaging category in 2024, with reported losses totaling $5.7 billion, a 24% increase from 2023 [2].

- Imposter Scams: Imposter scams ranked as the second-highest source of reported losses, amounting to $2.95 billion [2].

- Preferred Payment Methods for Fraudsters: In 2024, fraudsters predominantly leveraged bank transfers and cryptocurrency, accounting for more losses than all other payment methods combined [2].

- Common Fraud Categories: Imposter scams were the most frequently reported fraud category, followed by online shopping issues. Business and job opportunities also saw substantial losses, reaching $750.6 million [2].

- Exploitation of Job Seekers: Job and employment agency scams have seen a dramatic rise, with reports tripling between 2020 and 2024, and consumer losses escalating from 90millionto501 million [2].

- Organizational Vulnerability: The 2025 AFP Payments Fraud and Control Survey revealed that 79% of organizations were targets of payments fraud attacks or attempts in 2024, highlighting the widespread nature of the threat to businesses [3].

Emerging Fraud Trends

The landscape of financial fraud is continuously evolving, driven by technological advancements and the ingenuity of criminals:

- AI-Enhanced Scams: The proliferation of generative AI is enabling the creation of more sophisticated and convincing scams, making it harder for individuals to distinguish legitimate communications from fraudulent ones [4].

- Cryptocurrency and Digital Asset Fraud: The increasing adoption of cryptocurrencies has led to a resurgence in related fraud schemes, including pump-and-dump operations, fake Initial Coin Offerings (ICOs), and exchange hacks [4].

- Deepfakes: The emergence of deepfake technology poses a significant threat, particularly in authorized push payment (APP) scams, where criminals can impersonate individuals to authorize fraudulent transactions [5].

- Faster Payments, Faster Fraud: The advent of instant payment systems, while beneficial for legitimate transactions, also facilitates quicker execution of fraudulent activities, making recovery more challenging [6].

- Organized Crime Involvement: Organized crime rings are increasingly responsible for a majority of fraud attempts, indicating a shift towards more structured and coordinated criminal enterprises [7].

These statistics and trends paint a stark picture of the challenges posed by cybercrime and financial fraud in the digital era. The sheer volume of attacks, the escalating financial losses, and the continuous evolution of criminal tactics necessitate a robust and adaptive response, with forensic accounting playing a pivotal role in this ongoing battle.

The Role of Forensic Accounting in Combating Cybercrime and Financial Fraud

In the face of escalating cybercrime and financial fraud, forensic accounting has become an indispensable weapon in the arsenal of law enforcement, corporations, and legal entities. Forensic accountants leverage their unique blend of accounting, auditing, and investigative skills to unravel complex financial schemes, identify perpetrators, quantify damages, and provide expert testimony in legal proceedings. Their role extends beyond traditional financial analysis, delving deep into digital footprints and employing advanced techniques to combat modern forms of financial misconduct.

Key Functions of Forensic Accountants

Forensic accountants perform a variety of critical functions in combating cybercrime and financial fraud:

- Fraud Detection and Investigation: This is the core function. Forensic accountants are trained to identify red flags and anomalies in financial records that may indicate fraudulent activity. They conduct thorough investigations, often starting with a hypothesis of fraud and systematically gathering evidence to prove or disprove it. This involves analyzing large datasets, performing reconciliations, and interviewing witnesses.

- Digital Forensics and Data Analysis: With the shift to digital transactions, forensic accountants increasingly rely on digital forensics. They extract, preserve, and analyze electronic data from various sources, including computers, mobile devices, cloud storage, and network logs. Advanced data analytics tools are employed to identify patterns, trends, and outliers that might signify fraudulent behavior or cyber intrusions. This includes using specialized software for e- discovery, data mining, and link analysis.

- Tracing Illicit Funds: A crucial aspect of combating financial crime is tracing the flow of illicit funds. Forensic accountants meticulously follow money trails, often across multiple accounts, jurisdictions, and even through complex financial instruments like cryptocurrencies. This involves analyzing bank statements, wire transfers, credit card transactions, and blockchain ledgers to identify the origin, movement, and destination of fraudulent proceeds.

- Damage Quantification: In cases of fraud or cyberattacks, forensic accountants are responsible for quantifying the financial losses incurred by victims. This involves assessing direct losses, business interruption losses, reputational damage, and potential future losses. Their objective and evidence-based assessment of damages is critical for legal claims, insurance recoveries, and restitution orders.

- Expert Witness Testimony: Forensic accountants often serve as expert witnesses in legal proceedings. They translate complex financial information into clear, understandable terms for judges and juries. Their testimony, supported by their investigative findings and analysis, can be pivotal in securing convictions or favorable judgments in civil and criminal cases.

- Fraud Prevention and Risk Management: Beyond investigation, forensic accountants also play a proactive role in helping organizations strengthen their internal controls, identify vulnerabilities, and implement robust fraud prevention programs. They conduct risk assessments, develop fraud detection policies, and provide training to employees on recognizing and reporting suspicious activities.

Methodologies and Techniques

To effectively combat cybercrime and financial fraud, forensic accountants employ a range of specialized methodologies and techniques:

- Financial Statement Analysis: Scrutinizing financial statements for inconsistencies, unusual trends, or deviations from industry norms that might indicate manipulation or misrepresentation.

- Transaction Flow Analysis: Mapping the movement of funds through various accounts and entities to identify suspicious transactions, shell companies, or money laundering activities.

- Data Mining and Predictive Analytics: Utilizing sophisticated software to sift through vast amounts of financial data, identify hidden patterns, and predict potential fraud risks. Machine learning algorithms are increasingly being used to detect anomalies that human analysts might miss.

- Network Analysis: In cybercrime investigations, forensic accountants collaborate with cybersecurity experts to analyze network traffic, system logs, and digital artifacts to understand how a breach occurred, what data was compromised, and how the attack was executed.

- Interviewing and Interrogation Techniques: Employing specialized communication skills to gather information from witnesses, suspects, and other relevant parties. This requires an understanding of human behavior and legal protocols.

- Due Diligence: Conducting comprehensive financial investigations before mergers, acquisitions, or significant investments to identify undisclosed liabilities, potential fraud, or other financial risks.

- Blockchain Analysis: For cryptocurrency-related fraud, forensic accountants use specialized tools to analyze public blockchain ledgers, trace transactions, and identify wallet addresses associated with illicit activities. This is a rapidly evolving area requiring continuous learning.

Collaboration and Interdisciplinary Approach

Combating cybercrime and financial fraud effectively requires a collaborative and interdisciplinary approach. Forensic accountants often work closely with:

- Law Enforcement Agencies: Providing financial expertise and evidence to support criminal investigations and prosecutions.

- Cybersecurity Professionals: Collaborating to understand the technical aspects of cyberattacks, identify vulnerabilities, and secure digital evidence.

- Legal Counsel: Assisting attorneys in preparing for litigation, understanding financial evidence, and developing legal strategies.

- Internal Audit Teams: Working with internal auditors to strengthen organizational controls and improve fraud detection mechanisms.

- Regulatory Bodies: Assisting regulatory agencies in enforcing compliance and investigating violations of financial regulations.

This collaborative ecosystem is essential for a holistic response to the complex and interconnected nature of modern financial crime. The forensic accountant acts as a crucial bridge between the financial, legal, and technological domains, translating complex data into actionable intelligence for various stakeholders.

Case Studies and Real-World Examples

The theoretical frameworks and methodologies of forensic accounting are best understood through their application in real- world scenarios. The following case studies, ranging from historical financial frauds to contemporary cybercrimes, illustrate the critical role forensic accountants play in uncovering misconduct, quantifying damages, and supporting legal proceedings.

Beat Your Deadline

Hire a Writer Today!

✅ Get Your Assignment Done by Experts

Famous Financial Fraud Cases and Forensic Accounting’s Role

Enron Scandal (2001): This remains one of the most infamous corporate frauds in history. Enron, once a leading energy company, collapsed due to a complex web of accounting deceptions. Forensic accountants meticulously unraveled the intricate financial manipulations, which involved off-balance-sheet entities and fabricated financial records designed to hide billions in debt and inflate profits. Their work was crucial in exposing how top executives, including CEO Jeffrey Skilling and CFO Andrew Fastow, orchestrated the fraud, leading to their convictions and significant prison sentences. The Enron case underscored the necessity of forensic accounting in scrutinizing complex financial structures and holding corporate leaders accountable [8].

Tesco Accounting Scandal (2014): The UK supermarket giant Tesco faced a major scandal when forensic accountants discovered that the company had overstated its profits by hundreds of millions of pounds. This was achieved by prematurely recognizing income and delaying the recognition of costs. The forensic investigation revealed a deliberate attempt by executives to manipulate financial statements to meet profit targets and boost bonuses. The findings led to substantial fines, criminal charges against senior executives, and a significant drop in the company’s market value. This case highlighted the importance of forensic accountants in ensuring the integrity of financial reporting, even in large, established corporations [8].

Bernie Madoff’s Ponzi Scheme: Bernard Madoff orchestrated the largest Ponzi scheme in history, defrauding thousands of investors of billions of dollars over decades. Forensic accountants were instrumental in dissecting the elaborate fraud, which involved paying returns to existing investors with funds from new investors, rather than from actual profits. Their painstaking analysis of financial records, bank statements, and investment portfolios helped to reconstruct the fraudulent scheme, quantify the immense losses, and identify the victims. Madoff’s conviction and 150-year prison sentence were a direct result of the irrefutable financial evidence compiled by forensic experts [8].

Tyco International Scandal: This case involved the misappropriation of hundreds of millions of dollars by top executives, including CEO Dennis Kozlowski and CFO Mark Swartz. Forensic investigations revealed that they used company funds for lavish personal expenses, disguised as employee loan schemes, and concealed these activities from shareholders and regulators. Forensic accountants meticulously traced the illicit financial flows and exposed the fraudulent accounting practices, leading to the conviction of Kozlowski and Swartz on multiple charges. This case demonstrated the power of forensic accounting in uncovering executive misconduct and asset misappropriation [8].

WorldCom Fraud (2002): WorldCom, a telecommunications giant, engaged in an accounting fraud that involved improperly classifying billions of dollars in operating expenses as capital expenditures. This manipulation artificially inflated the company’s assets and profits. Forensic accountants played a pivotal role in uncovering these accounting irregularities, which ultimately led to the company’s bankruptcy and the conviction of several top executives, including CEO Bernard Ebbers, who received a 25-year prison sentence. The WorldCom case emphasized the need for rigorous scrutiny of accounting classifications and the devastating impact of financial statement fraud [8].

Cybercrime and Financial Fraud: Contemporary Challenges

While the above cases illustrate traditional financial fraud, the digital era introduces new complexities, often intertwining cybercrime with financial misconduct. Forensic accountants are increasingly involved in investigations related to:

- Ransomware Attacks: These attacks involve encrypting an organization’s data and demanding a ransom, often in cryptocurrency. Forensic accountants work alongside cybersecurity experts to assess the financial impact, trace the flow of cryptocurrency payments (even on pseudonymous blockchains), and quantify business interruption losses. Their expertise is vital in understanding the financial motivations behind such attacks and in potential recovery efforts [8].

- Business Email Compromise (BEC) Scams: BEC scams are sophisticated phishing attacks where criminals impersonate executives or trusted vendors to trick employees into making fraudulent wire transfers. Forensic accountants are crucial in these cases for tracing the diverted funds across multiple bank accounts, often in different jurisdictions. They analyze transaction data, identify intermediary accounts, and collaborate with law enforcement to freeze and recover stolen funds. The speed and global nature of these scams necessitate rapid forensic financial analysis [8].

- Data Breaches and Identity Theft: When data breaches expose sensitive personal and financial information, they often lead to identity theft and subsequent financial fraud. Forensic accountants quantify the financial losses suffered by individuals and organizations due to fraudulent credit card use, unauthorized account access, and other related crimes. They assist victims in recovering funds, assess damages for legal claims, and help organizations implement stronger preventative measures [8].

- Cryptocurrency Fraud: The rise of cryptocurrencies has opened new avenues for fraud, including pump-and-dump schemes, fraudulent Initial Coin Offerings (ICOs), and direct theft from exchanges. Forensic accountants with specialized knowledge in blockchain analysis are increasingly in demand. They use analytical tools to trace illicit cryptocurrency transactions across public ledgers, identify associated wallet addresses, and link them to real-world identities when possible. This emerging area requires continuous adaptation of forensic techniques to keep pace with technological advancements [8].

These diverse case studies underscore the evolving nature of financial crime and the indispensable role of forensic accounting. Whether it’s unraveling complex corporate accounting schemes or tracing digital currency in a cyberattack, the ability of forensic accountants to meticulously analyze financial data, identify irregularities, and present findings in a clear and legally defensible manner is paramount to combating fraud in the digital era.

Visualizing the Impact: Cybercrime and Fraud Losses

To further illustrate the escalating impact of cybercrime and financial fraud, consider the following visualizations based on recent data:

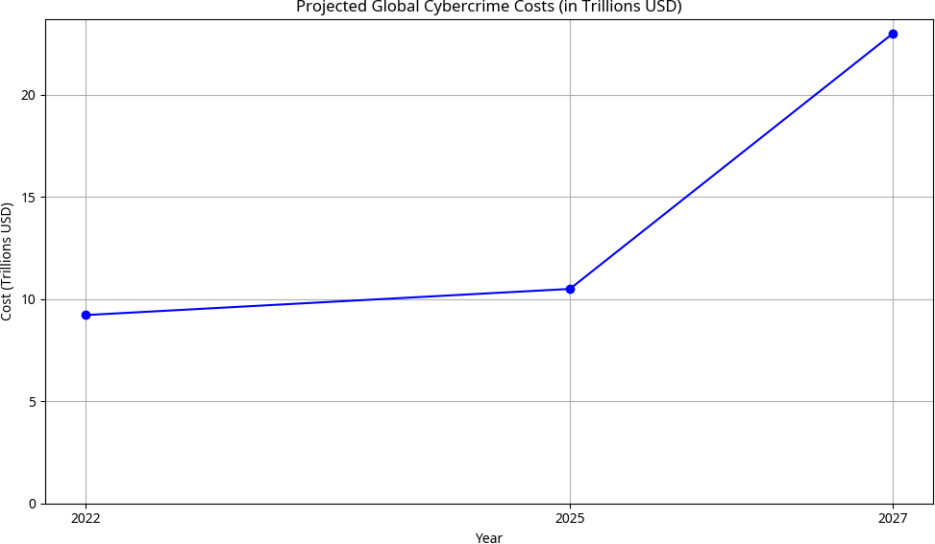

Projected Global Cybercrime Costs (in Trillions USD)

This graph highlights the alarming trajectory of cybercrime costs, projected to reach 10.5 trillion annually by 2025 and further escalating to 23 trillion by 2027. This upward trend underscores the growing financial burden cybercrime places on the global economy.

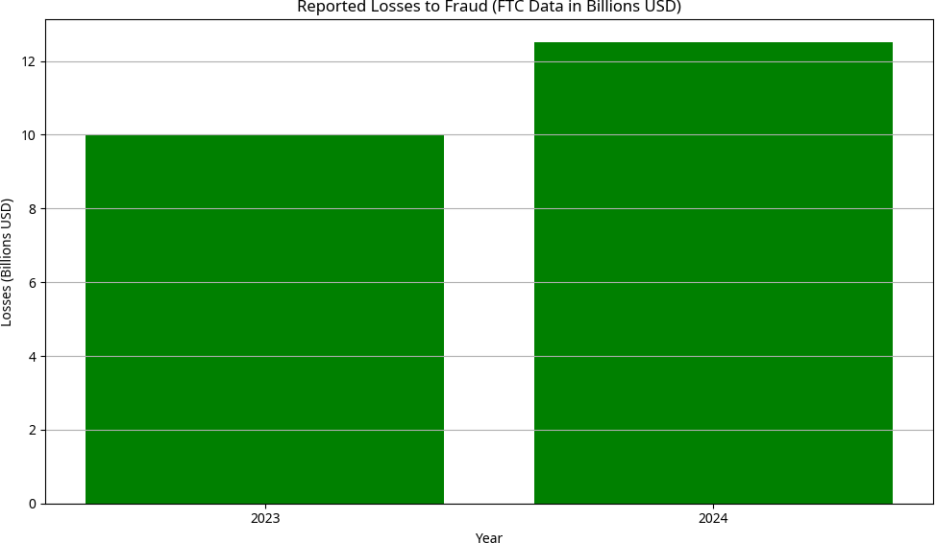

Reported Losses to Fraud (FTC Data in Billions USD)

This bar chart illustrates the significant increase in reported losses to fraud, as per FTC data. The jump from 10 billion in 2023 to 12.5 billion in 2024 signifies a substantial rise in the financial impact of fraudulent activities on consumers.

These visualizations reinforce the urgent need for robust forensic accounting practices and cybersecurity measures to mitigate these escalating financial threats.

Challenges and Opportunities for Forensic Accounting

The digital era, while amplifying the need for forensic accounting, also presents a unique set of challenges and opportunities for the profession. Navigating this complex landscape requires continuous adaptation, innovation, and a forward-thinking approach.

Challenges

Volume and Velocity of Data: The sheer volume of digital data generated daily is immense. Forensic accountants must contend with petabytes of information from diverse sources, making it challenging to identify, collect, and analyze relevant evidence efficiently. The velocity at which this data is generated also means that investigations must be conducted rapidly to prevent evidence from being altered or destroyed.

Data Complexity and Variety: Digital data comes in various formats and from numerous platforms, including structured databases, unstructured text, social media, and IoT devices. This complexity requires specialized tools and expertise to process and interpret, often necessitating collaboration with data scientists and IT specialists.

Evolving Cybercrime Tactics: Cybercriminals are constantly innovating, developing new attack vectors and sophisticated methods to evade detection. This includes the use of advanced persistent threats (APTs), polymorphic malware, and increasingly, AI-driven attacks that can mimic human behavior, making traditional detection methods less effective.

Jurisdictional Challenges: Financial fraud and cybercrime often transcend national borders, involving perpetrators and victims in different countries. This raises complex jurisdictional issues, requiring international cooperation, adherence to diverse legal frameworks, and navigating varying data privacy regulations.

Anonymity of Cryptocurrencies: While blockchain technology offers transparency, the pseudonymous nature of cryptocurrency transactions can make it challenging to link digital wallets to real-world identities. This anonymity is often exploited by criminals for money laundering and illicit financing, posing a significant hurdle for tracing funds.

Talent Gap: There is a growing demand for forensic accountants with expertise in digital forensics, cybersecurity, and data analytics. However, a shortage of professionals possessing this specialized skill set creates a talent gap, making it difficult for organizations to adequately staff their fraud prevention and investigation teams.

Maintaining Objectivity and Independence: In high-stakes investigations, forensic accountants must maintain strict objectivity and independence, especially when dealing with internal fraud cases or disputes involving powerful entities. This requires adherence to ethical guidelines and professional standards.

Opportunities

Technological Advancements: The same technological advancements that enable cybercrime also offer powerful tools for forensic accountants. Artificial intelligence (AI) and machine learning (ML) can be leveraged for predictive analytics, anomaly detection, and automated data analysis, significantly enhancing the efficiency and effectiveness of investigations. Robotic Process Automation (RPA) can automate routine tasks, freeing up forensic accountants to focus on more complex analytical work.

Big Data Analytics: The ability to process and analyze large datasets (Big Data) provides an unprecedented opportunity to uncover hidden patterns, relationships, and anomalies that would be impossible to detect manually. This allows for more comprehensive and proactive fraud detection.

Blockchain Analysis Tools: Specialized blockchain analytics tools are continuously evolving, offering enhanced capabilities to trace cryptocurrency transactions, identify suspicious activities, and potentially de-anonymize illicit financial flows. This presents a significant opportunity for forensic accountants to expand their expertise into the burgeoning crypto space.

Increased Demand for Services: The escalating rates of cybercrime and financial fraud have led to a surge in demand for forensic accounting services across various sectors, including corporate, legal, government, and insurance. This creates significant career opportunities and growth for the profession.

Proactive Fraud Prevention: Beyond reactive investigations, forensic accountants have a growing opportunity to play a proactive role in designing and implementing robust fraud prevention frameworks. This includes developing advanced internal controls, conducting regular risk assessments, and providing training on fraud awareness and detection.

Specialization and Niche Markets: The complexity of digital financial crime encourages specialization within forensic accounting. Professionals can develop expertise in areas such as cryptocurrency investigations, cyber insurance claims, data breach response, or specific industry frauds, opening up niche markets and specialized consulting opportunities.

International Collaboration: The cross-border nature of cybercrime necessitates greater international collaboration. Forensic accountants have an opportunity to work with global law enforcement agencies, regulatory bodies, and multinational corporations to develop coordinated strategies for combating transnational financial crime.

By embracing these opportunities and proactively addressing the challenges, forensic accounting can continue to evolve as a vital discipline in safeguarding financial integrity in the digital age. The future of the profession lies in its ability to integrate cutting-edge technology with traditional investigative acumen, fostering a new generation of digitally-savvy forensic experts.

Conclusion

The digital era has irrevocably transformed the landscape of financial transactions, bringing with it both unprecedented opportunities and formidable challenges in the form of sophisticated cybercrime and financial fraud. In this dynamic environment, forensic accounting has emerged as an indispensable discipline, evolving from its traditional roots to embrace cutting-edge technologies and methodologies. The pervasive nature and escalating costs of cyberattacks and financial scams underscore the critical need for skilled forensic accountants who can navigate the complexities of digital evidence, trace illicit funds across borders and through cryptocurrencies, and provide expert insights in legal proceedings.

As demonstrated by historical cases like Enron and Madoff, and contemporary threats such as ransomware and BEC scams, the ability of forensic accountants to meticulously analyze financial data, identify irregularities, and present findings in a clear and legally defensible manner is paramount. They serve as a crucial bridge between the financial, legal, and technological domains, collaborating with law enforcement, cybersecurity professionals, and legal counsel to ensure justice and protect economic integrity.

However, the profession faces ongoing challenges, including the overwhelming volume and complexity of digital data, the constantly evolving tactics of cybercriminals, and the jurisdictional complexities of cross-border fraud. Despite these hurdles, technological advancements in AI, machine learning, and blockchain analytics offer significant opportunities for forensic accountants to enhance their investigative capabilities and contribute to more proactive fraud prevention strategies. The increasing demand for their specialized services further highlights the growing recognition of their vital role.

In essence, forensic accounting in the digital era is not merely about numbers; it is about uncovering narratives of deception, holding perpetrators accountable, and ultimately, safeguarding the trust and stability of our global financial systems. As technology continues to advance, the role of the forensic accountant will only become more critical, requiring continuous learning, adaptation, and a steadfast commitment to ethical investigation in the relentless fight against cybercrime and financial fraud.

Beat Your Deadline

Hire a Writer Today!

✅ Get Your Assignment Done by Experts

References

[1] AAG IT Services. (2025, June). The Latest Cyber Crime Statistics (updated June 2025). Retrieved from https://aag-it.com/the-latest-cyber-crime-statistics/

[2] Federal Trade Commission. (2025, March 10). New FTC Data Show a Big Jump in Reported Losses to Fraud to $12.5 Billion in 2024. Retrieved from https://www.ftc.gov/news-events/news/press-releases/2025/03/new-ftc-data-show-big-jump-reported-losses-fraud-125-billion-2024

[3] AFP. (2025). 2025 AFP Payments Fraud and Control Survey Report. Retrieved from https://www.financialprofessionals.org/training-resources/resources/survey-research-economic-data/details/payments-fraud

[4] ACFE Insights Blog. (2025). Top 5 Fraud Trends of 2025. Retrieved from https://www.acfe.com/acfe-insights-blog/blog-detail?s=top-fraud-trends-2025

[5] Verafin. (2025, January 9). Fraud Trends & Technology: 5 Inflection Points for 2025. Retrieved from https://verafin.com/2025/01/fraud-trends-technology-5-inflection- points-for-2025/

[6] Jack Henry. (2025, March 31). 2025 Fraud Trends: Protecting Against Emerging Threats. Retrieved from https://www.jackhenry.com/fintalk/2025-fraud-trends-protecting-against-emerging-threats

[7] Alloy. (2025). Alloy’s 2025 State of Fraud Report. Retrieved from https://www.alloy.com/fraud-report-2025

[8] Apollo Solutions. (2023, March 15). Uncovering fraud: famous Forensic Accounting cases that rocked the world. Retrieved from https://www.apollo-solutions.com/resources/blog/uncovering-fraud-famous-forensic-accounting-cases-that-rocked-the-world/

Leave a Reply